If you’re thinking of buying a home, you’re probably wondering what you need to save for your down payment. Is it 20% of the loan, or could you put down less? While there are lower down payment programs available that allow qualified buyers to put down as little as 3.5%, it’s important to understand the many perks that come with a 20% down payment.

Here are four reasons why putting 20% down may be a great option if it works within your budget.

1. Your Interest Rate May Be Lower

A 20% down payment vs. a 3-5% down payment shows your lender you’re more financially stable and not a large credit risk. The more confident your lender is in your credit score and your ability to pay your loan, the lower the mortgage interest rate they’ll likely be willing to give you.

2. You’ll End Up Paying Less for Your Home

The larger your down payment, the smaller your loan amount will be for your mortgage. If you’re able to pay 20% of the cost of your new home at the start of the transaction, you’ll only pay interest on the remaining 80%. If you put down 5%, the additional 15% will be added to your loan and will accrue interest over time. This will end up costing you more over the lifetime of your home loan.

3. Your Offer Will Stand Out in a Competitive Market

In a market where many buyers are competing for the same home, sellers often like to see offers come in with 20% or larger down payments. The seller gains the same confidence as the lender in this scenario. You are seen as a stronger buyer with financing that’s more likely to be approved. Therefore, the deal will be more likely to go through.

4. You Won’t Have To Pay Private Mortgage Insurance (PMI)

What is PMI? According to Freddie Mac:

“For homeowners who put less than 20% down, Private Mortgage Insurance or PMI is an added insurance policy for homeowners that protects the lender if you are unable to pay your mortgage.

It is not the same thing as homeowner’s insurance. It’s a monthly fee, rolled into your mortgage payment, that’s required if you make a down payment less than 20%. . . . Once you’ve built equity of 20% in your home, you can cancel your PMI and remove that expense from your monthly payment.”

As mentioned earlier, if you put down less than 20% when buying a home, your lender will see your loan as having more risk. PMI helps them recover their investment in you if you’re unable to pay your loan. This insurance isn’t required if you’re able to put down 20% or more.

Many times, home sellers looking to move up to a larger or more expensive home are able to take the equity they earn from the sale of their house to put 20% down on their next home. With the equity homeowners have today, it creates a great opportunity to put those savings toward a larger down payment on a new home.

Bottom Line

If you’re looking to buy a home, consider the benefits of 20% down versus a smaller down payment option. Let’s connect so you have expert advice to help make your homeownership goals a reality.

Chrysti Tovani is a Fair Oaks Real Estate Advisor, Transition Specialist, and the author of Downsizing with Intention. She helps homeowners sell long held homes, downsize with clarity, and navigate major life transitions with confidence and strategic guidance.

With decades of experience in real estate, mortgage, and title, Chrysti brings deep industry knowledge and thoughtful preparation to every transaction. Her approach blends strategic home marketing, skilled negotiation, and emotional intelligence, ensuring that each move is handled with both precision and care.

As the founder of I Love Fair Oaks, a hyperlocal media platform highlighting trusted businesses and community life in Fair Oaks, California, Chrysti has built an integrated authority ecosystem that connects real estate expertise with community leadership.

Her work centers on clarity, visibility, and long term legacy, helping clients move forward with confidence while strengthening the community she serves.

![Why It’s So Important To Hire a Pro [INFOGRAPHIC]](https://chrystitovani.com/wp-content/uploads/2022/09/20220909-KCM-Share-549x300-1.png)

![Why It’s So Important To Hire a Pro [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2022/09/08160644/20220909-KCM-Share-549x300.png)

If you’re following along with the news today, you’re probably hearing a lot about record-breaking home prices, rising consumer costs, supply chain constraints, and more. And if you’re thinking about purchasing a home this year, all of these inflationary concerns are likely making you wonder if you should wait to buy. Investopedia explains that during […]

If you’re following along with the news today, you’re probably hearing a lot about record-breaking home prices, rising consumer costs, supply chain constraints, and more. And if you’re thinking about purchasing a home this year, all of these inflationary concerns are likely making you wonder if you should wait to buy. Investopedia explains that during […]

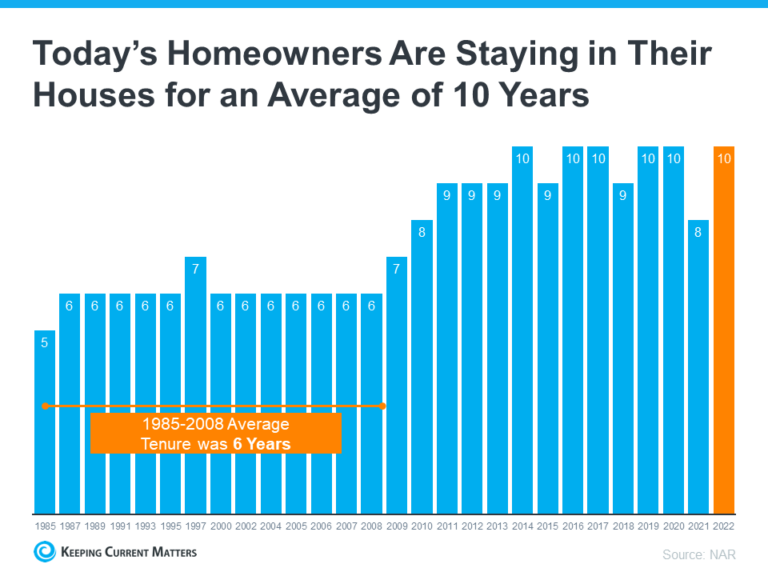

A new year brings with it the opportunity for new experiences. If that resonates with you because you’re considering making a move, you’re likely juggling a mix of excitement over your next home and a sense of attachment to your current one.

A new year brings with it the opportunity for new experiences. If that resonates with you because you’re considering making a move, you’re likely juggling a mix of excitement over your next home and a sense of attachment to your current one.